As we head into the winter months, gas prices and availability become a higher priority for many businesses and households. In this month’s review we’ll be looking at the factors set to dictate how gas prices move over the coming season.

October started with fear in the energy markets as Iran launched retaliatory strikes against Israel. Worries of the conflict expanding have been a repetitive theme in energy markets for the past year and it seemed as though that was unlikely to change.

The increased military activity had led to rising prices, however, as the month progressed, hopes of a possible ceasefire have increased with leadership on both sides signalling they may be willing to put an end to hostilities. How this plays out over the coming days and weeks could be a key factor in the stability of energy prices throughout the coming winter.

Meteorological forecasts have now confirmed that the UK is likely to see a La Niña winter. La Niña weather patterns refer to cooling oceans and strong winds which will have an impact on British conditions. During La Niña winters it is more likely that the UK will see a cold start to winter, a milder end, and a wet Spring. A milder end to winter would bring relief and take any pressure of the gas reserves which are currently close to being 100% full. The current forecasts make it seem unlikely that a winter of sustained cold temperatures (when compared to historic averages) is forthcoming.

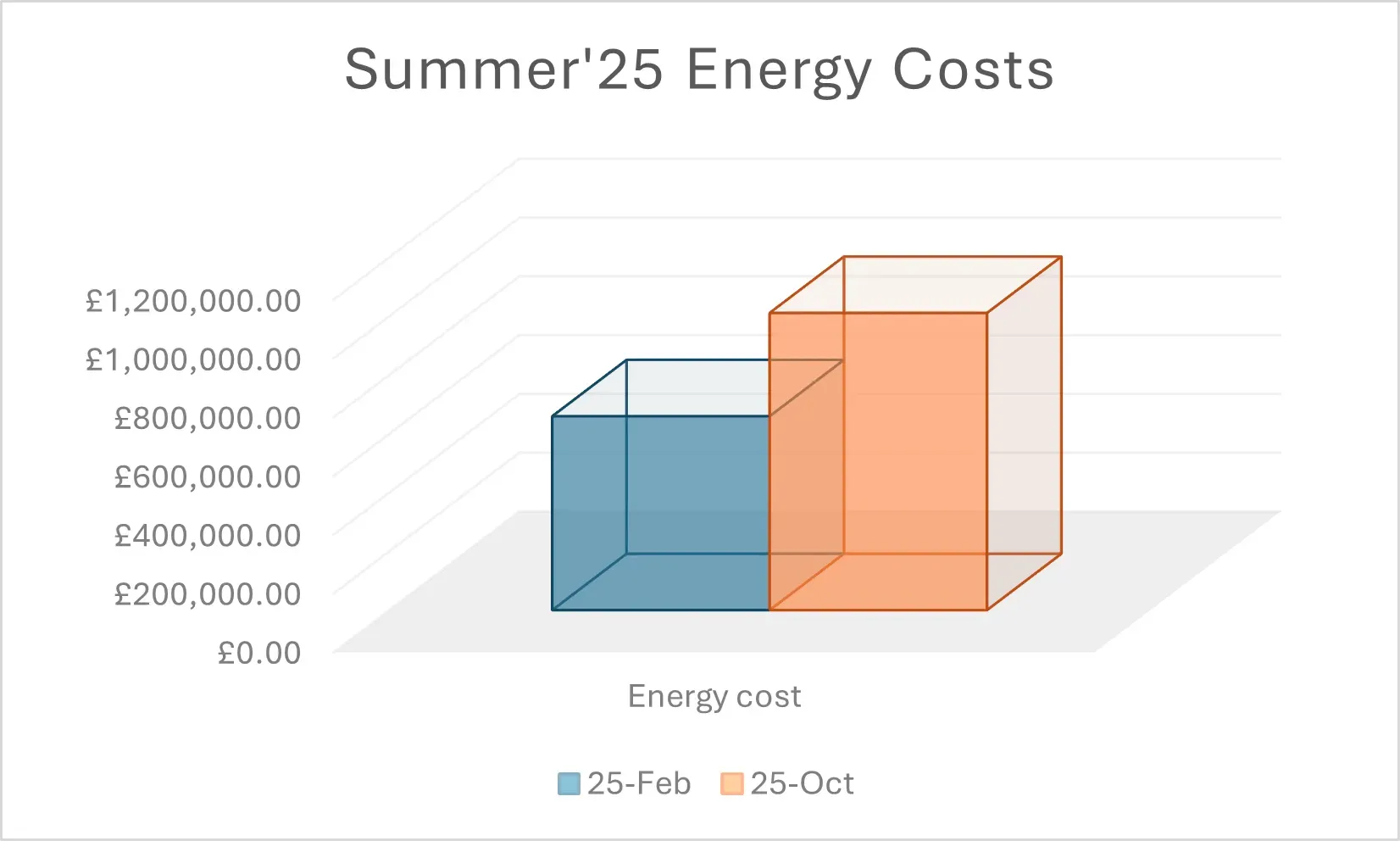

A POWWR energy report released in October has shown that business energy spending is increasing with businesses using 4.1% more energy during the past quarter. Energy prices remain a key concern for many high-consuming industries. Since the end of February, prices have been steadily rising. The wholesale energy prices for gas on October 31st were more than 80% higher than they were in late February.

For a manufacturing business with a 3GWh summer consumption, the difference between purchasing next summer’s energy back in February compared to today, is a difference of approximately £350k.