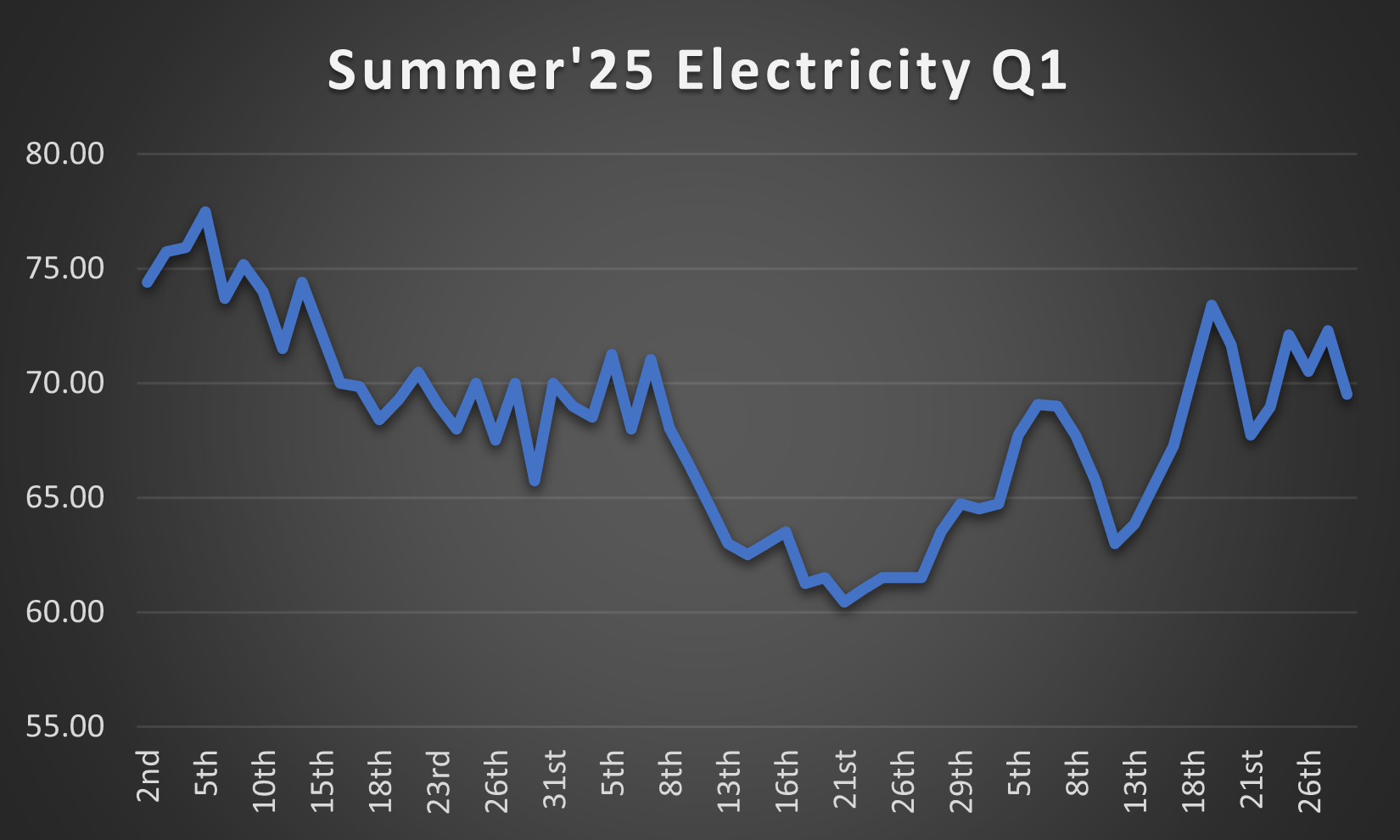

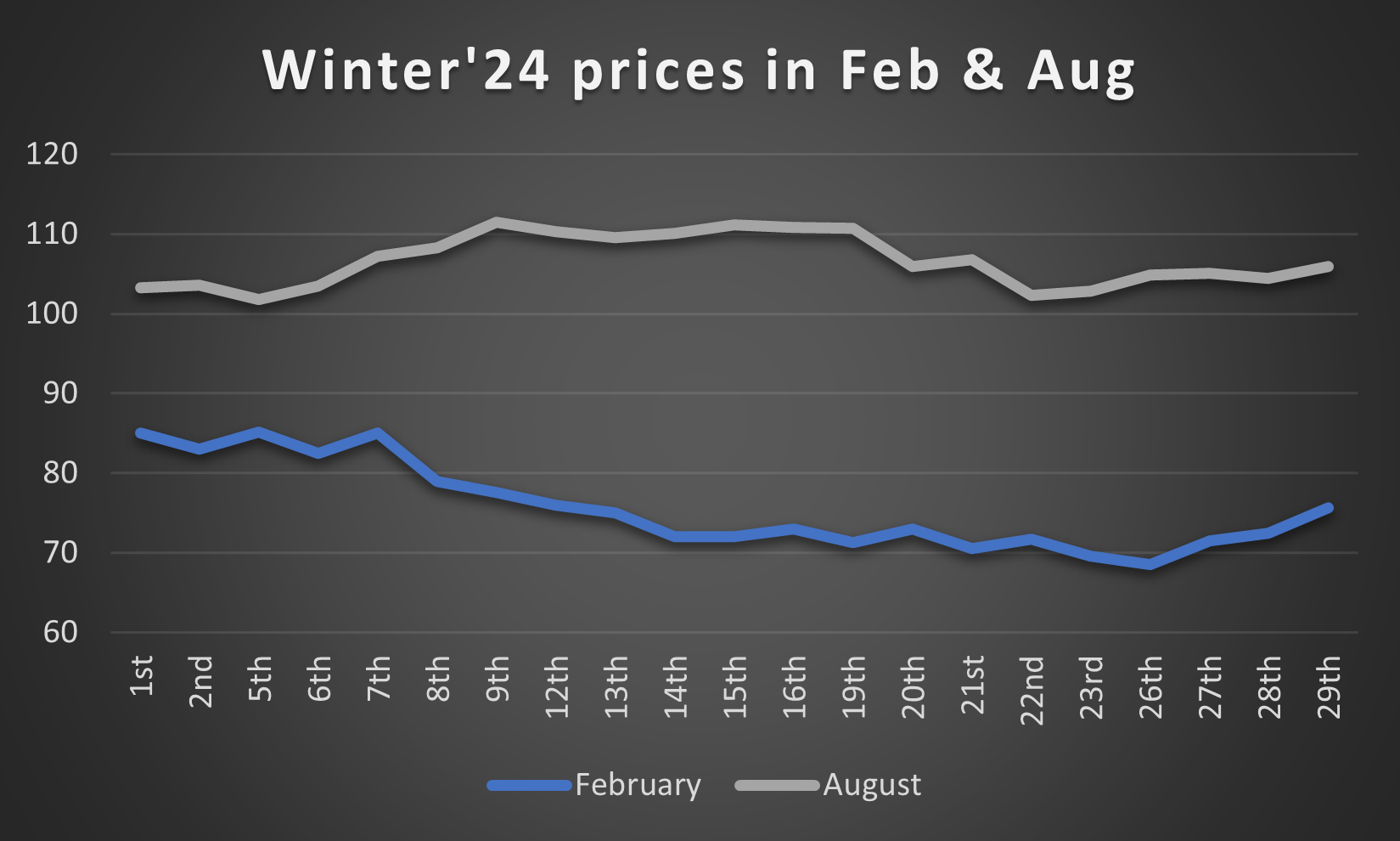

With consumer spending declining and OFGEM raising their price cap, you would be forgiven for seeing February as a month where negative news was at the forefront, but in the energy markets, this was not the case.

Should I Use an Energy Broker/Partner? With energy markets becoming increasingly complex and volatile, many UK businesses are asking the same question: is it worth using an energy broker/ partner? While it’s possible to manage energy procurement and administration in-house, doing so effectively requires time, expertise, and constant market awareness. For many organisations, working with a specialist partner can unlock significant savings and remove a substantial administrative burden. Smarter Procurement and Market Timing One of the primary reasons businesses engage an energy broker is procurement . Securing a competitive contract is about far more than simply comparing prices at renewal. A competent energy broker will monitor wholesale markets daily, advise on the best time to contract, provide access to a wide range of suppliers and contract structures, and tailor strategies based on your budgetary needs. This dedicated market insight can help businesses avoid locking into contracts during market peaks and instead secure energy when conditions are more favourable. Invoice Validation: Are You Being Overcharged? Energy billing is notoriously complex, and errors are more common than many businesses realise. Without proper scrutiny, overcharges can go unnoticed for months or even years. A good energy partner will validate invoices against contract terms allowing them to identify incorrect charges or discrepancies. They will then contact your supplier to recover historical overpayments ensuring that you haven’t paid more than necessary and your team don’t have to use their time in dealing with suppliers. This ongoing oversight ensures you only ever pay what you should, not what you’re billed. Support with Suppliers, DNOs and Disputes Dealing with energy suppliers and network operators can be time-consuming and, at times, frustrating. Whether it’s billing disputes, contract queries, or technical issues, having expert support can make a significant difference. An experienced broker can act as a single point of contact for suppliers, liaise with Distribution Network Operators (DNOs) , and support escalations -- including cases taken to the Energy Ombudsman. This not only saves time, but by having a team familiar with supplier’s SLAs, it ensures that issues are handled efficiently and with the right level of expertise. Specialist Cost Reduction Knowledge Beyond procurement, there are a number of technical areas where businesses can reduce costs, many of which are often overlooked. These include: kVA capacity reviews to ensure you’re not overpaying for unused capacity TCR banding optimisation , which can significantly impact network charges Identifying opportunities to reduce consumption or shift usage patterns Without specialist knowledge, these areas are easy to miss, but -- with the right guidance -- they can deliver meaningful savings without any operational disruption. Is It the Right Choice for Your Business? For smaller businesses with limited time and resource, an energy broker can provide immediate value. For larger organisations with complex portfolios, the benefits are often even greater -- particularly when it comes to validation, optimisation, and strategic planning. By having experienced external support, a business can feel confident that their energy spend is being scrutinised and managed with the correct level of attention, without having to divert the focus of employees whose time could be better spent in other areas. Take Control of Your Energy Strategy At SeeMore Energy, we work as a true partner to our clients. By combining market expertise, technical insight, and ongoing support, we help businesses reduce costs and stay in control of their energy strategy. From procurement and invoice validation to kVA reviews and dispute management, we ensure every aspect of your energy is working as efficiently as possible. If you’re unsure whether you’re getting the best deal -- or simply want peace of mind -- get in touch today. Our expert team will help you identify savings, reduce risk, and take control of your energy costs.